Shout Out to PCS Title for one of the most exacting blog posts about Florida real estate trends. Thanks again!

Wenston DeSue

|

|

|

|

|

|

Shout Out to PCS Title for one of the most exacting blog posts about Florida real estate trends. Thanks again!

Wenston DeSue

|

|

|

|

|

|

Florida has become a place of over-inflated pricing and unaffordable housing. However, the media continues to drive buyer decision-making. Wenston DeSue

Index: North Port and Naples are in top 5 of 1Q 2022 emerging housing markets as Fla. continues to attract migration from other states. They were top 2 in 4Q 2021.

NEW YORK – In the first quarter of 2022, less expensive cities with strong local economies climbed The Wall Street Journal/Realtor.com Emerging Housing Markets Index, which could be another sign that many home buyers are giving priority to affordability.

In recent years, fast-rising housing prices have pushed buyers from expensive coastal cities into cheaper housing markets, as remote-work opportunities have expanded and people search for different lifestyles during the pandemic.

Economists say that as house prices and mortgage rates continue to increase, more people are expected to migrate. “People are chasing affordability," said Sam Khater, chief economist at Freddie Mac.

The Rapid City, South Dakota, metro area of about 145,000 people near the Wyoming border was the top-ranked market for the quarter. It was followed by Santa Cruz, California; North Port, Florida; Santa Rosa, California; and Naples, Florida.

The top 20 cities in the ranking have an average population size of about 600,000. The top-ranked markets in the first quarter had faster home sales, higher wages and shorter commute times than the market as a whole, said George Ratiu, manager of economic research at Realtor.com.

North Port and Naples were the top two markets in the fourth quarter and held in the top five as Florida continues to attract migration from other states.

Some of the top-ranked markets are also desirable vacation destinations, including Santa Cruz, Naples, and Coeur d’Alene, Idaho.

Source: Wall Street Journal (04/26/22) Friedman, Nicole

Index: North Port and Naples are in top 5 of 1Q 2022 emerging housing markets as Fla. continues to attract migration from other states. They were top 2 in 4Q 2021.

Index: North Port and Naples are in top 5 of 1Q 2022 emerging housing markets as Fla. continues to attract migration from other states. They were top 2 in 4Q 2021.

NEW YORK – In the first quarter of 2022, less expensive cities with strong local economies climbed The Wall Street Journal/Realtor.com Emerging Housing Markets Index, which could be another sign that many home buyers are giving priority to affordability.

In recent years, fast-rising housing prices have pushed buyers from expensive coastal cities into cheaper housing markets, as remote-work opportunities have expanded and people search for different lifestyles during the pandemic.

Economists say that as house prices and mortgage rates continue to increase, more people are expected to migrate. “People are chasing affordability," said Sam Khater, chief economist at Freddie Mac.

The Rapid City, South Dakota, metro area of about 145,000 people near the Wyoming border was the top-ranked market for the quarter. It was followed by Santa Cruz, California; North Port, Florida; Santa Rosa, California; and Naples, Florida.

The top 20 cities in the ranking have an average population size of about 600,000. The top-ranked markets in the first quarter had faster home sales, higher wages and shorter commute times than the market as a whole, said George Ratiu, manager of economic research at Realtor.com.

North Port and Naples were the top two markets in the fourth quarter and held in the top five as Florida continues to attract migration from other states.

Some of the top-ranked markets are also desirable vacation destinations, including Santa Cruz, Naples, and Coeur d’Alene, Idaho.

Source: Wall Street Journal (04/26/22) Friedman, Nicole

Real Estate

Wenston DeSue is a realtor, organizational consultant, design, construct, build expert and developmental networker. Real estate is the business of exchange and affects every person on the planet. Real estate on all levels represents resources, access and ultimately, power. Knowledge is power…

Housing markets continue to run hot, despite rising interest rates and home prices. Some researchers worry a fear of missing out may be fueling the current trend.

FORT LAUDERDALE, Fla. – Rising interest rates and higher home prices would normally cool a hot housing market, yet the national and local real estate scenes continue to run red hot.

Researchers at the Federal Reserve Bank of Dallas are concerned that a fear of missing out, colloquially known as FOMO, is creating a buying snowball effect that may lead to a housing bubble if left unchecked.

The current market, where higher prices and other factors are not resulting in a slowdown, is moving away from market fundamentals, they found, suggesting that buyer exuberance, in the form of fear of missing out, is driving the current trend.

“The resulting fundamental-driven higher house prices may have fueled a fear-of-missing-out wave of exuberance involving new investors and more aggressive speculation among existing investors,” said researchers.

“Expectations-driven explosive appreciation (often called exuberance) in real house prices has many consequences,” they went onto write, “including the misallocation of economic resources, distorted investment patterns, individual bankruptcies and broad macroeconomic effects on growth and employment.”

The paper then described how “this self-fulfilling mechanism leads to price growth that may become exponential (or explosive),” resulting in even greater misalignment, until policymakers intervene, investors become cautious, “or even a bust occurs.”

Locally, The market’s momentum is evidenced in astronomical price growth – the median sale price of a home in the tri-county area is $450,000, a 20% increase from the previous year, according to data from Redfin.

The biggest area of concern for researchers is how the housing market is diverging from basic market fundamentals like mortgage rates, inventory and income.

Researchers used datasets from the International Housing Observatory to find out whether buyer exuberance is playing a role in steep housing prices. From there, they marked what time periods had significant levels of buyer exuberance. Researchers warned that the last time the housing market saw such exuberance was before the crash of 2008.

When asked about the trend, Ken H. Johnson, real estate economist at Florida Atlantic University, said, “I think there are other factors, but this fear of missing out is amongst the most notable. We saw this around 2005 in Miami where people were buying and there was really no financial reason to buy.”

When it comes to consumers and their purchase decisions, emotions, either positive or negative, play one of the most important roles, said Dr. Khaled Aboulnasr at Florida Golf Coast University. Emotions can also cloud consumers’ perception when making decisions.

“Sometimes if you are unrealistically optimistic or if you have too much fear and anxiety, it may not let you weigh the true risk of the decision you are making,” added Aboulnasr.

Potential buyers have had to watch prices rise and housing availability drop, all while the rental market grew brutal. It all leads to frustration.

“At this point, they feel that it is more difficult, especially if you are applying for a mortgage, and they are at such a disadvantage to the cash buyer,” he said. “It becomes a much stronger motivator of behavior.” In other words, it’s tempting to think that if you get a chance at a house, you take it.

Additional motivations include missing out on lower mortgage rates, which can make a home more unaffordable as they rise, as well as the fear of not being able to save up for a home as rents rise.

Many buyers have watched as homes they once passed on for being too expensive have become even more expensive, leading them to fear that they may miss out on more equity gains if they wait out the housing market, added Whitney Dutton with the Dutton Group in Fort Lauderdale.

“People are less worried about finding that perfect home than they are worried about lose[ing] out,” said Dutton. “They are worried that if they don’t pay this [amount] now is it going to be more over-priced next year.”

The volatile rental market also adds to buyer fear. “There are people who have been renting for a couple years, thinking they were going to rent in the short term until prices came down. Now they think that’s not going to happen,” Dutton added. And as their buying opportunities have withered, landlords have raised rents aggressively – rents have risen upwards of 30% since last year, whereas a fixed-rate mortgage would have been relatively stable.

Though 2008 saw a bust, both nationally and locally, market forces are a bit different today. If any market correction should happen, Dallas researcher said, it won’t be of the magnitude of the last crash, mainly because the forces behind today’s market include low inventory, rather than excessive borrowing.

Florida Atlantic University researchers previously said that buying in the current boom could prove to be a risky decision, as homebuyers are potentially buying near the peak of the market, and it could take years before they see a return on their investment.

And it’s unlikely that a bust will happen in this current housing market for South Florida, though prices will eventually start to trend back to normal, said Ken H. Johnson, real estate economist with Florida Atlantic University.

“Some cities will fare differently,” he said. “If you live in an inventory shortage and expected population growth,” he said in describing South Florida, “I don’t think you will see a housing crash.”

Of their work indicating exuberance driving an imbalanced market, Federal Reserve Bank of Dallas economist Enrique Martinez Garcia made a medical analogy.

“The chances of providing a full remedy and minimize the impact on the patient are better when you are able to detect signs of the problem quickly and act earlier. Our base scenario would be, therefore, that greater awareness of the risk of unsustainable price growth can contribute to investors becoming more cautious about the prospects of continued price growth at the current rates.”

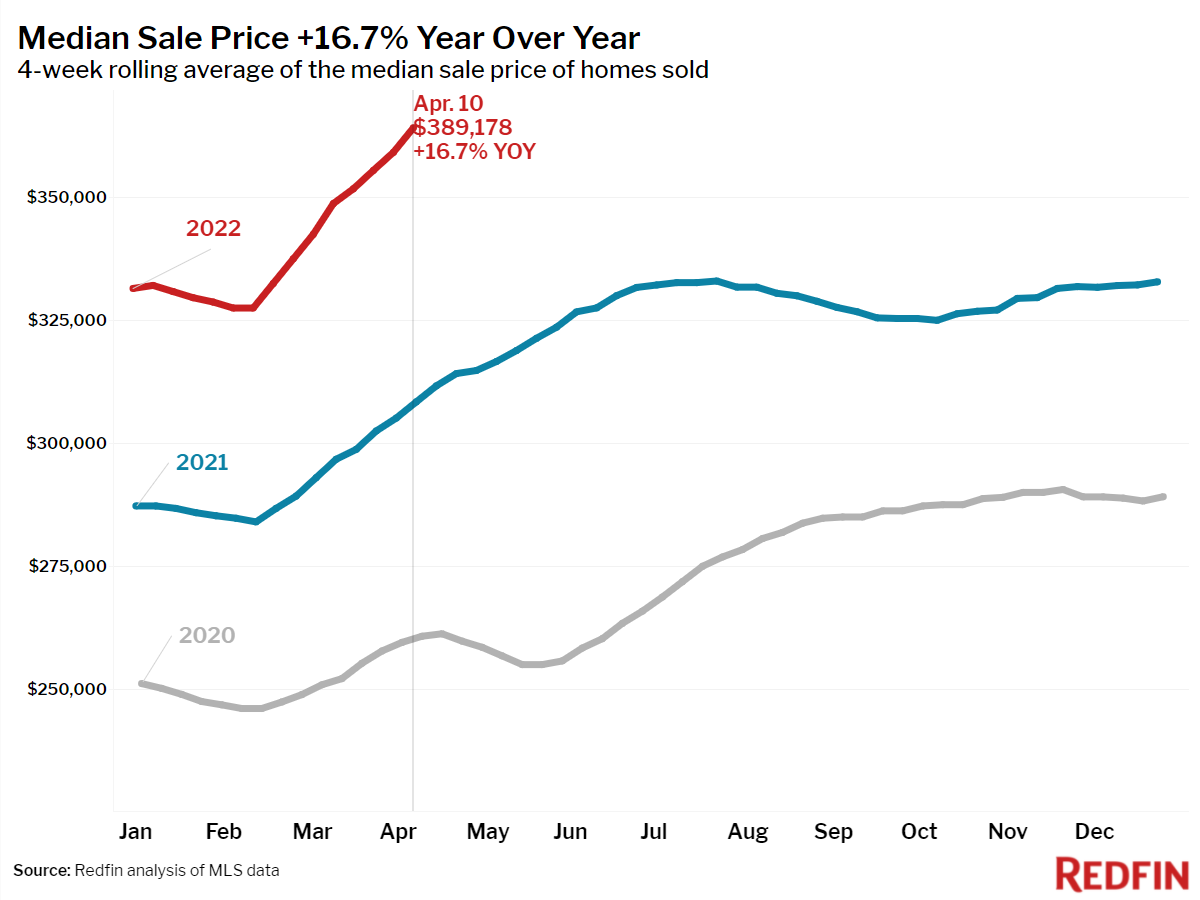

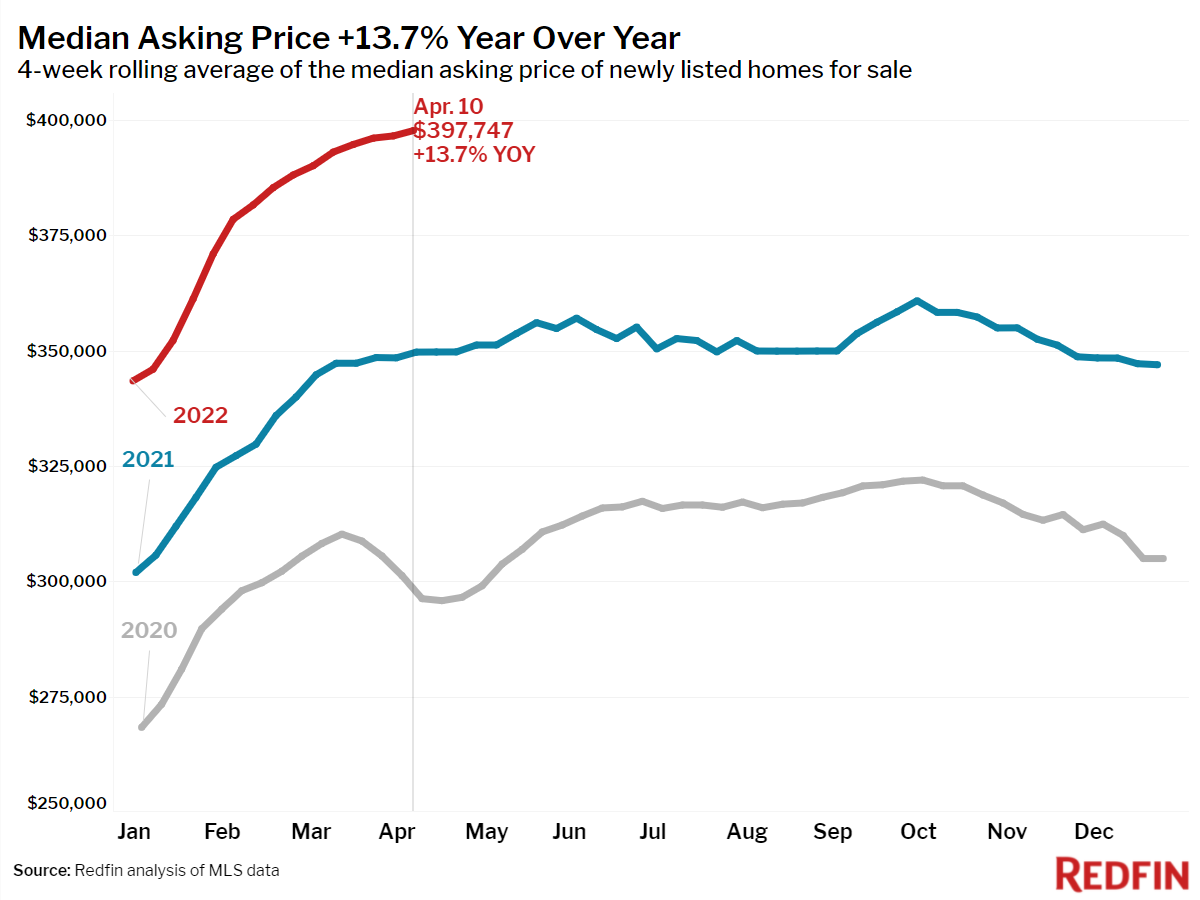

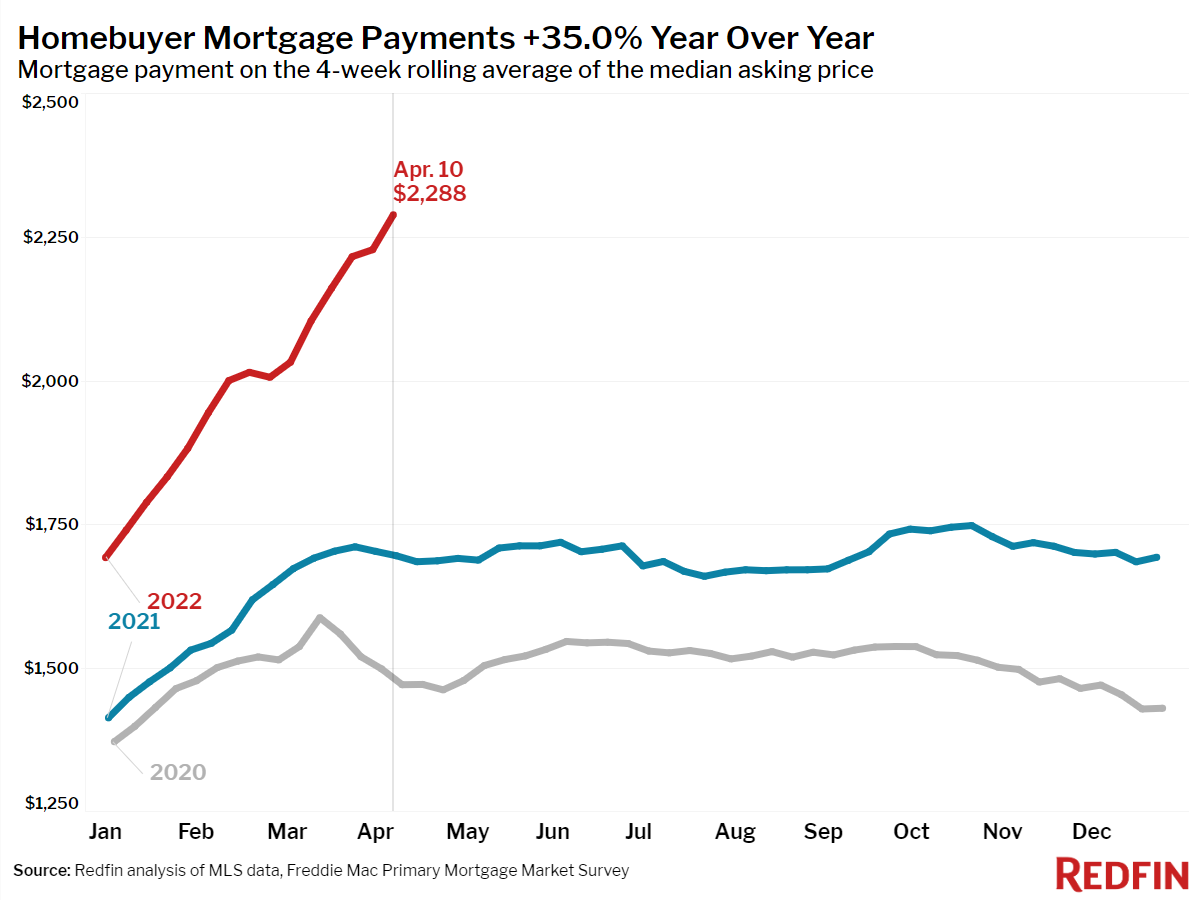

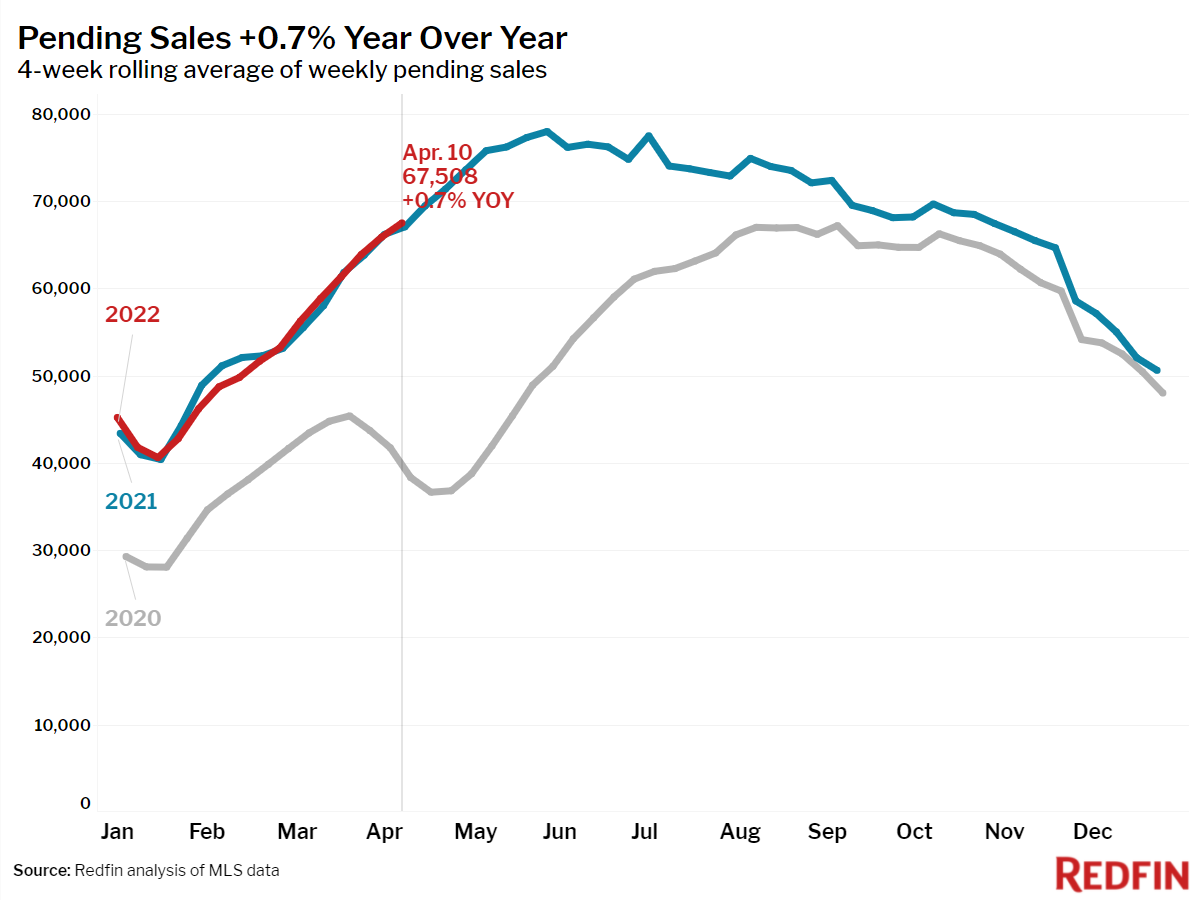

REDFIN speaks to a shift in housing prices in 2022.

Wenston DeSue

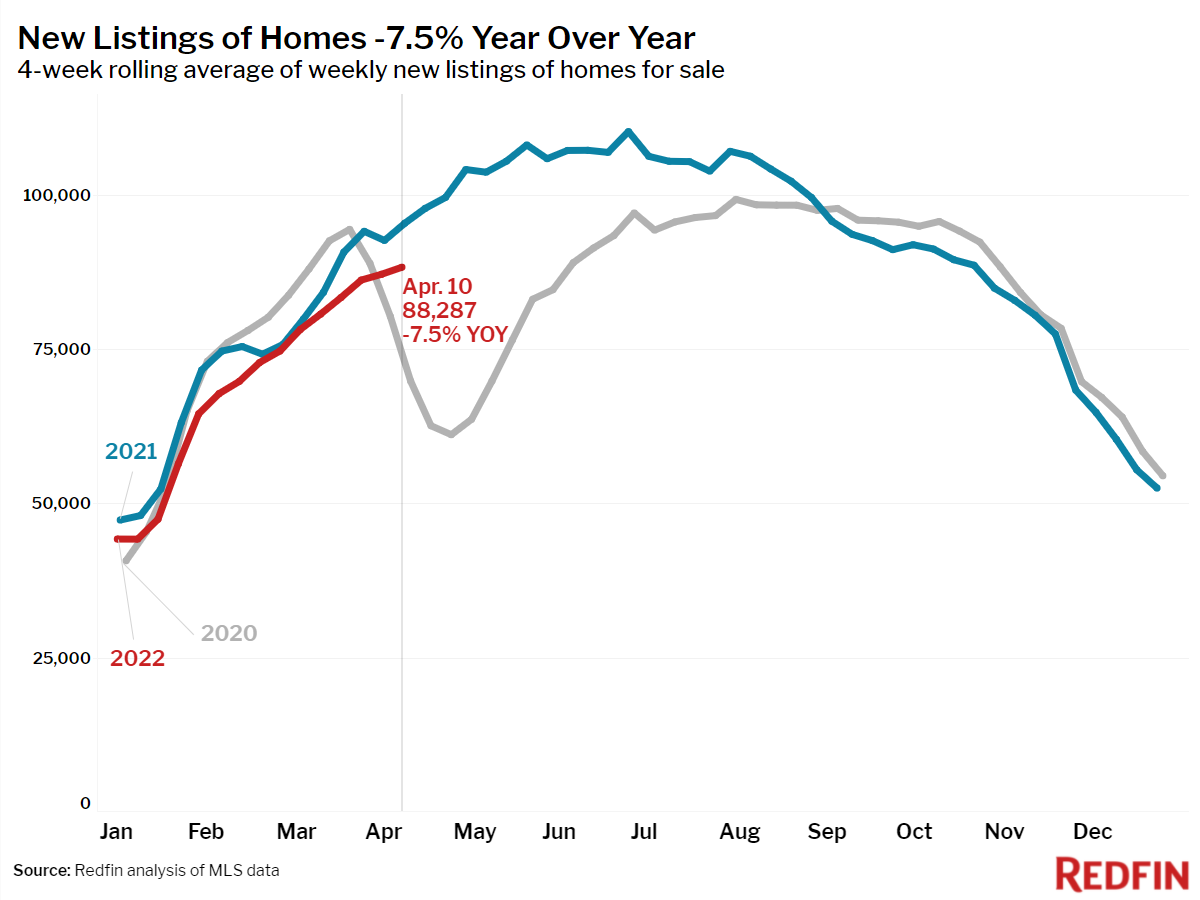

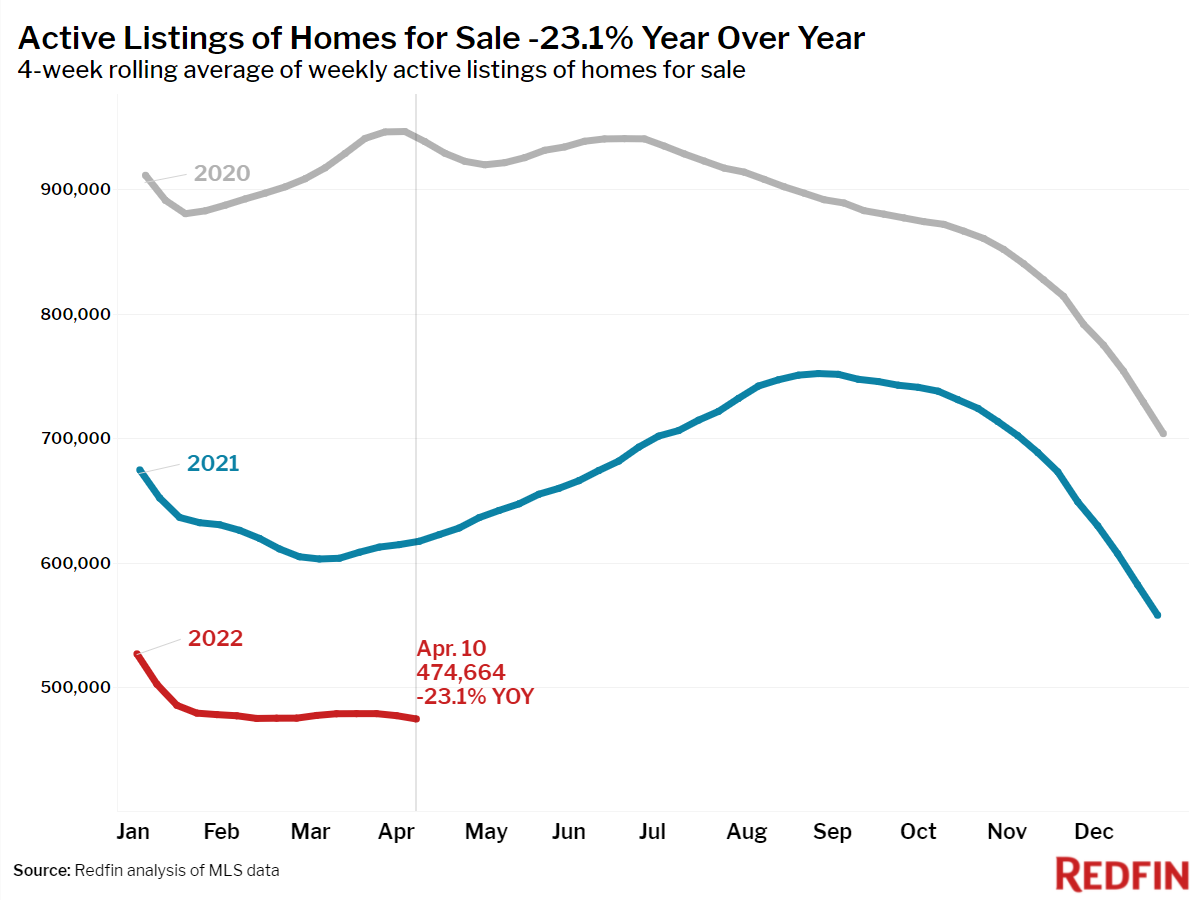

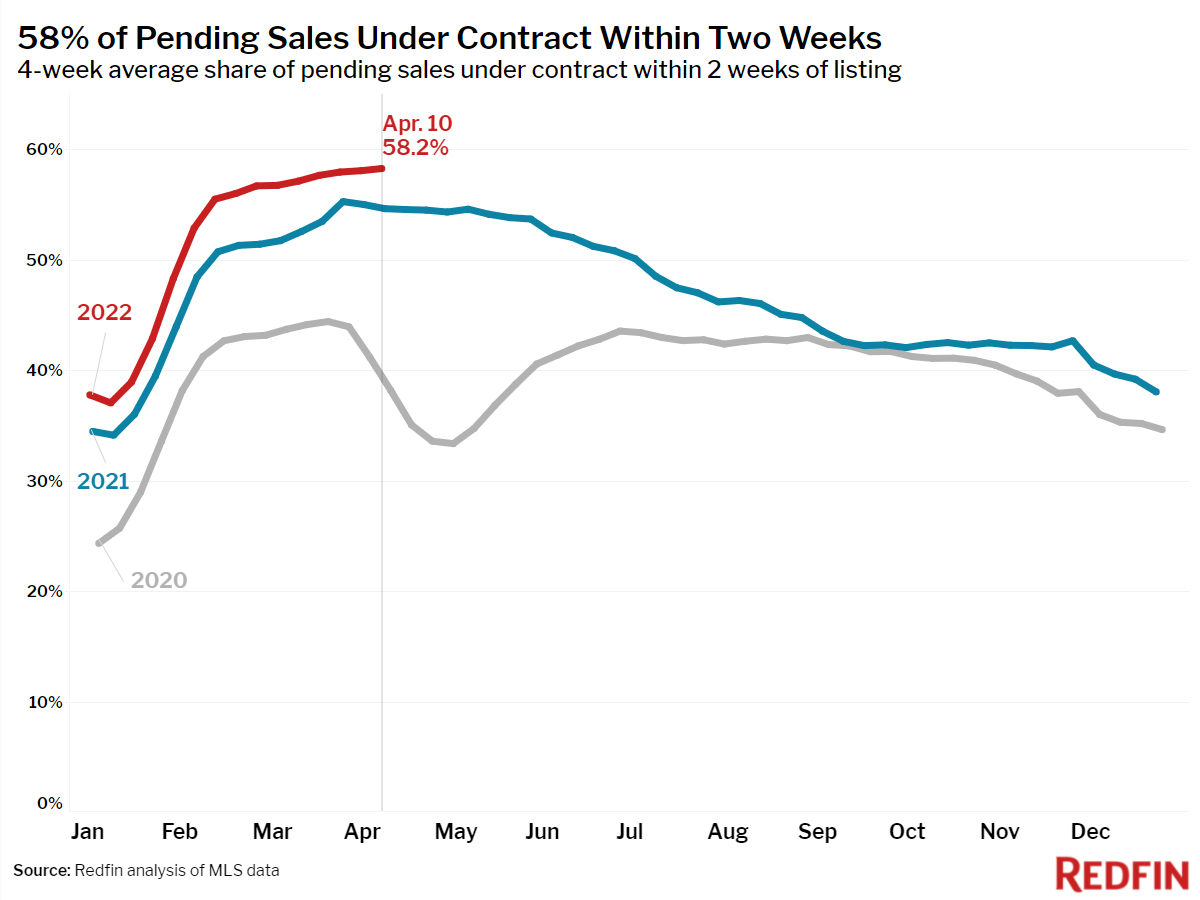

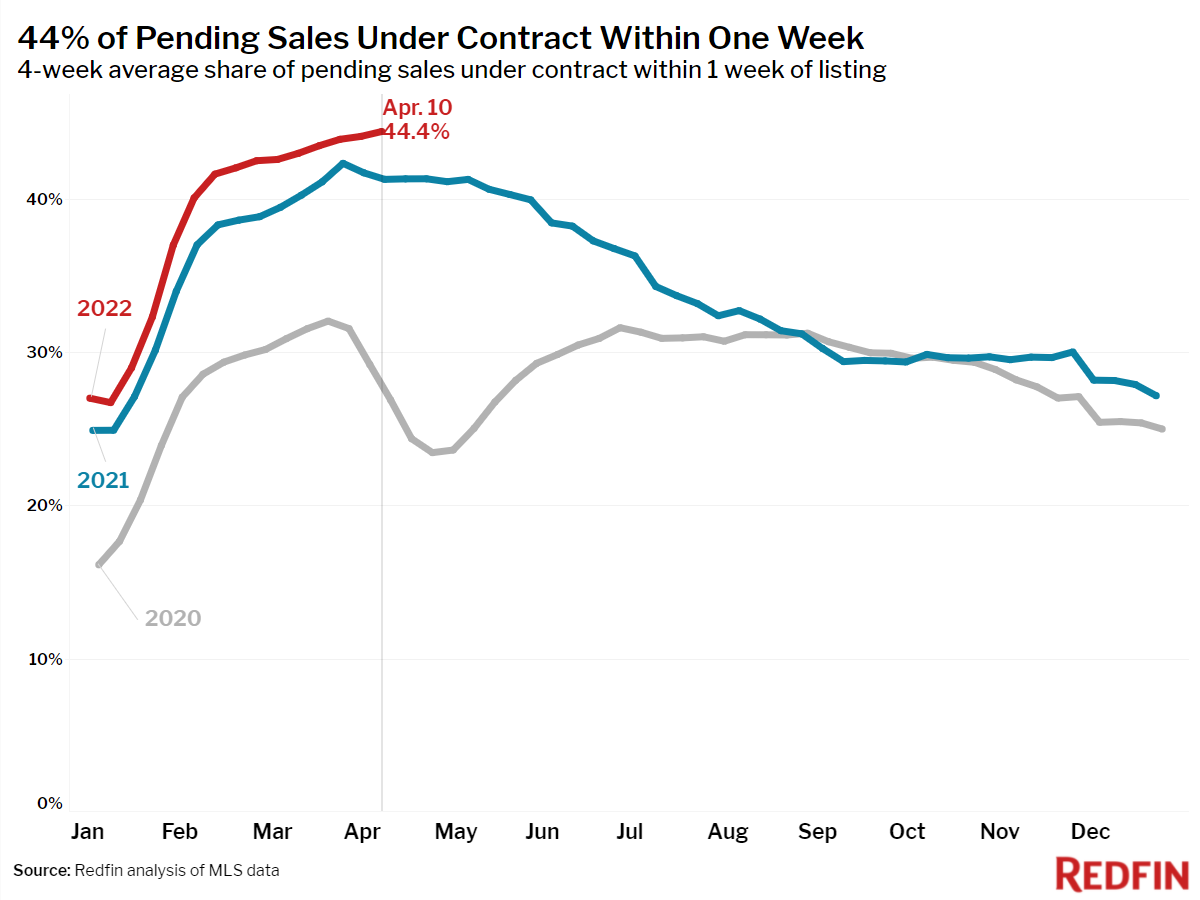

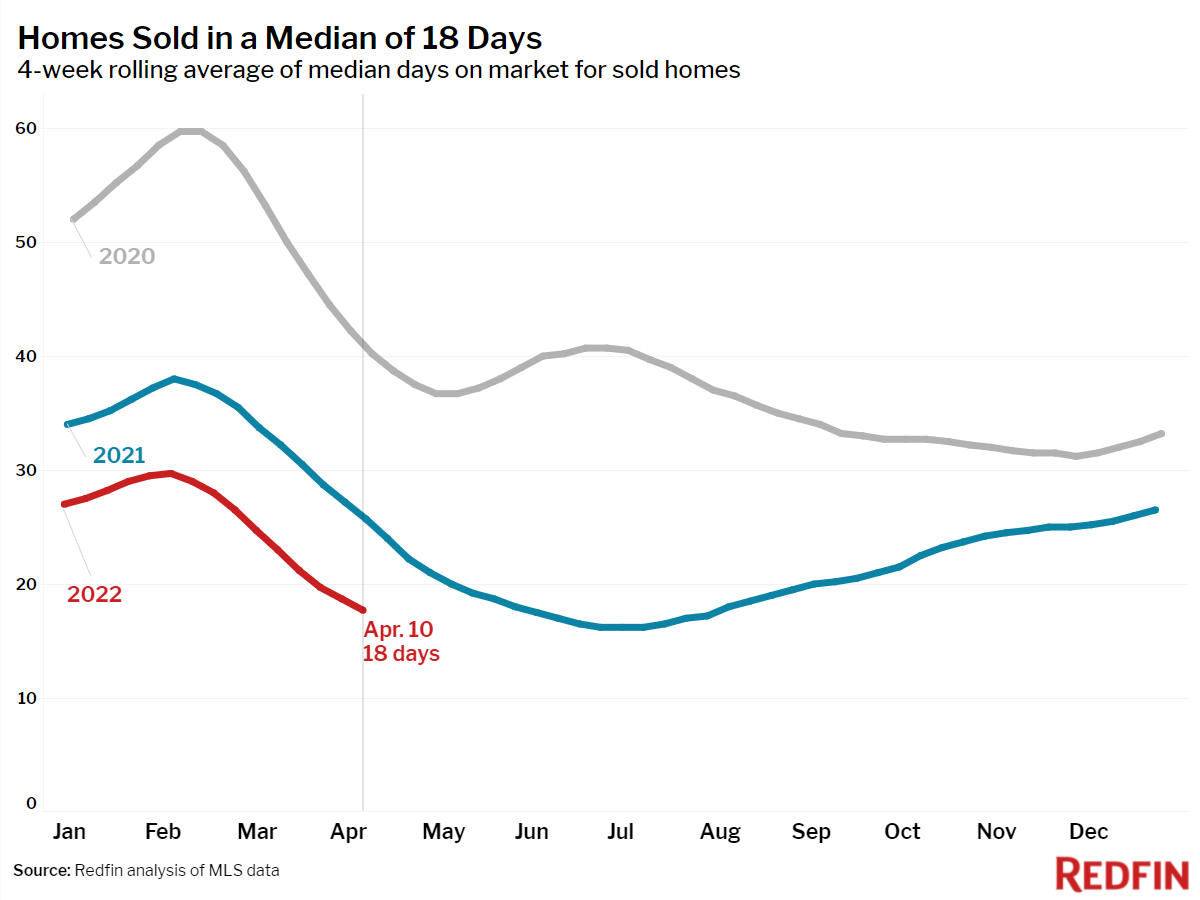

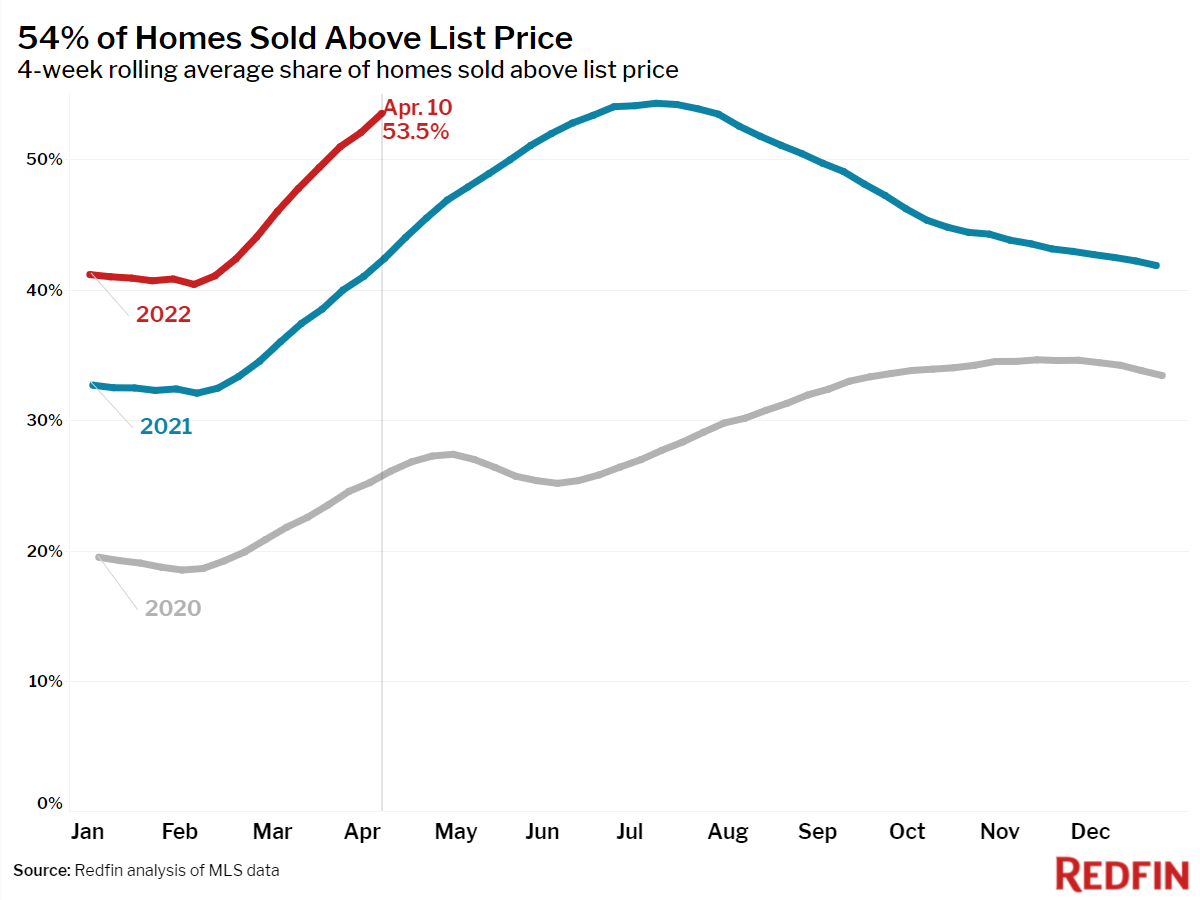

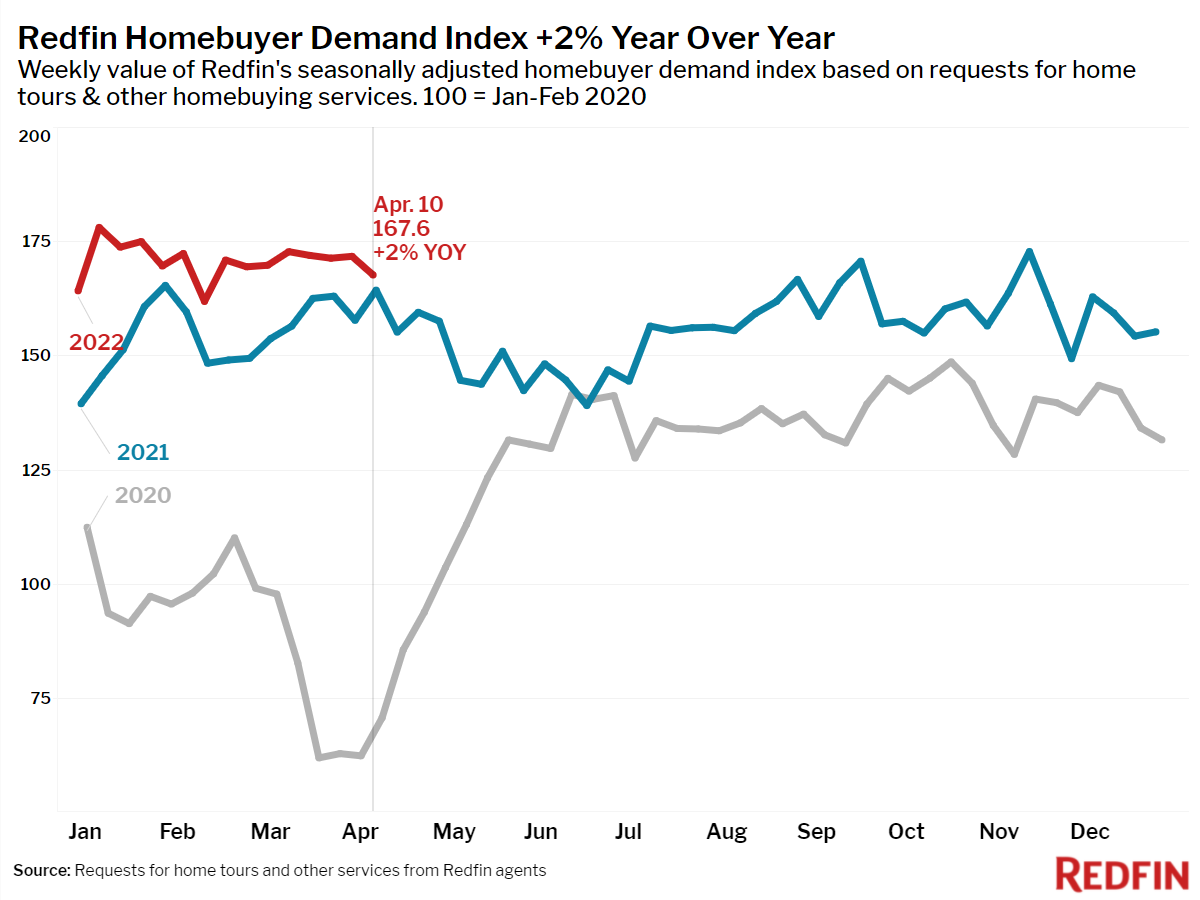

Early-stage homebuying demand continues to falter this spring as new listings fell 7% from a year earlier, the average 30-year fixed mortgage rate shot up to 5% and the median asking price climbed to $397,747, sending the typical homebuyer’s monthly payment up 35% year over year to an all-time high of $2,288. Here are the key early indicators that tell us demand is softening at a time of year it typically springs up:

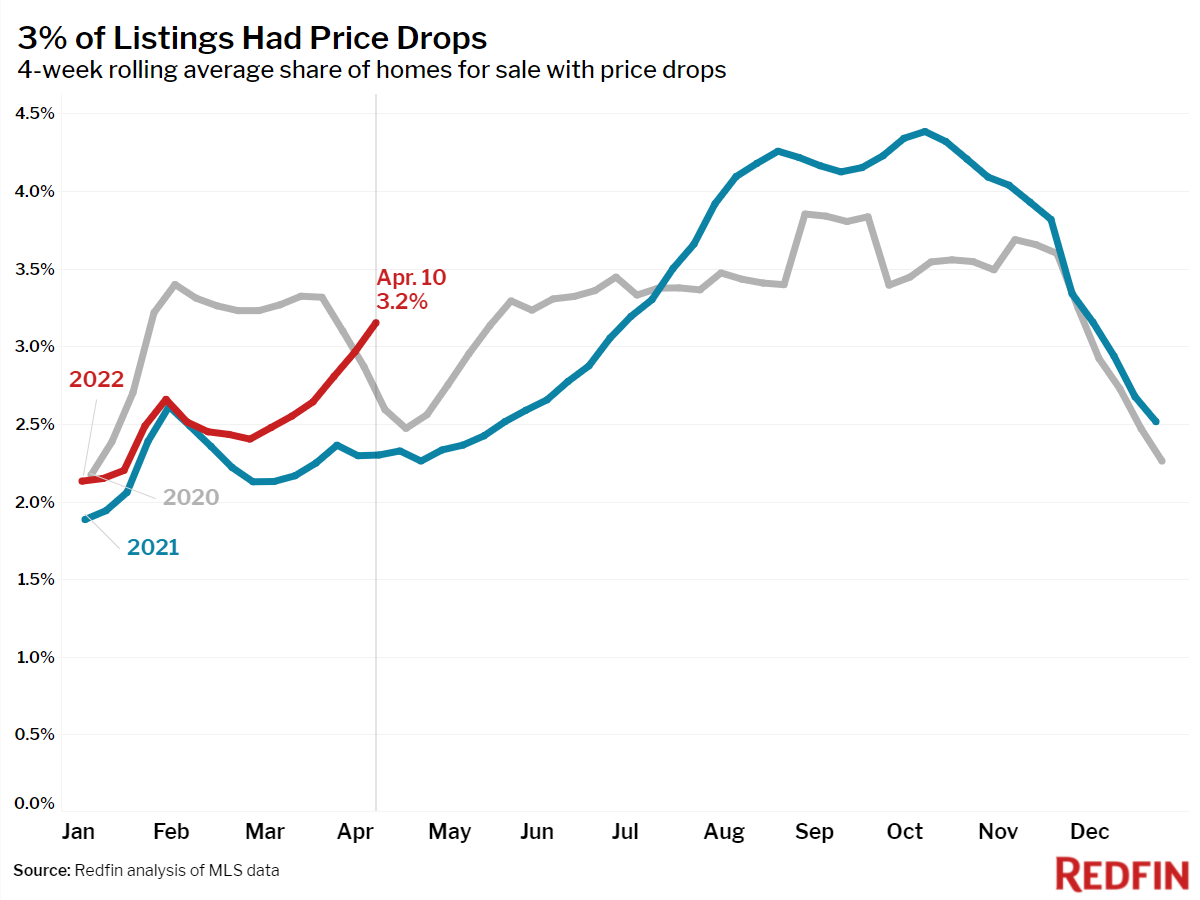

We’re also closely watching the accelerating share of home listings with price drops, which is climbing at its fastest spring pace since at least 2015, another sign that demand is not meeting sellers’ expectations.

“There really is a limit to homebuyer demand, even though the market over the past few years has made it seem endless,” said Redfin Chief Economist Daryl Fairweather. “The sharp increase in mortgage rates is pushing more homebuyers out of the market, but it also appears to be discouraging some homeowners from selling. With demand and supply both slipping, the market isn’t likely to flip from a seller’s market to a buyer’s market anytime soon.”

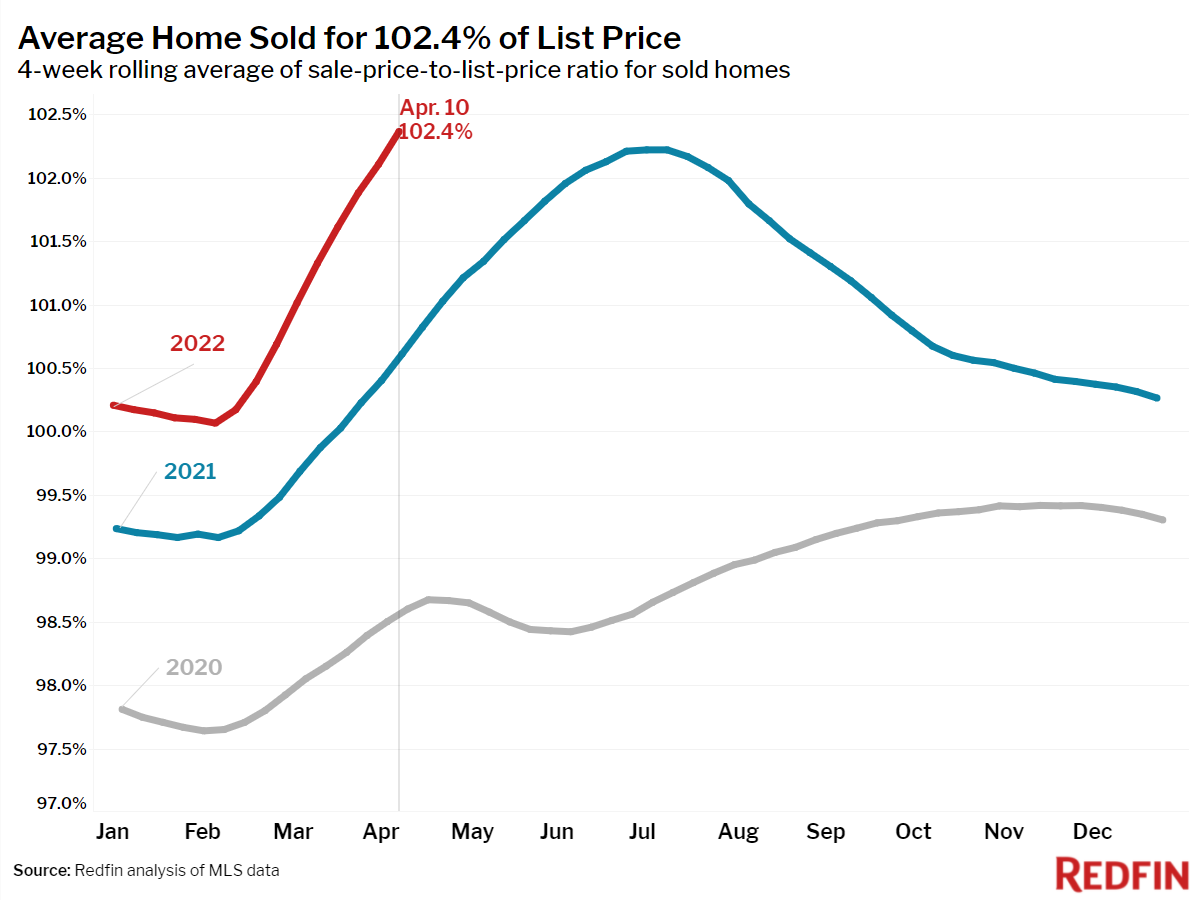

Despite these early signs that the market is slowing, it still feels as hot as ever for homebuyers, with new records set for home-selling speeds and price escalations, based on data going back to 2015. Forty-five percent of homes that went under contract found a buyer within one week, and the average home that sold went for 2.4% above its asking price.

“If a home is on the market for more than a week, people start to wonder why or assume something is wrong with it,” said Redfin Boston real estate agent James Gulden. “Every offer I’ve written recently has faced multiple offers, but some people have finally had enough of all the competition and are pulling out. They’re becoming less willing to make a risky offer in a high-stress bidding war situation.”

Unless otherwise noted, the data in this report covers the four-week period ending April 10. Redfin’s housing market data goes back through 2012.

Refer to our metrics definition page for explanations of all the metrics used in this report.

GOVERNMENT SHOULD DECIDE TO EITHER BE IN OR OUT OF PROVIDING THIS TYPE OF HOUSING…plausible deniability is avoidance…Wenston DeSue

While the US public housing system may have started off with the intention of providing quality homes to low income and vulnerable populations, those efforts were quickly dashed by how the program was created and managed.

Inadequate funding, poor maintenance, and media sensationalization helped create a narrative of substandard slum living, and the system set up to help so many hardly stood a chance. Here is how the public housing system was doomed to failure.

The foundation of the public housing system was faulty from the beginning

Public housing emerged as a concept in the 19th century largely as a response to the prevalence of densely-packed, substandard “slums” in urban areas. The idea was that the public sector was better equipped to serve low-income households than private landlords. The federal government was tasked with financing construction of public housing units where slums currently stood, and local housing authorities would put together development deals to ensure completion.

Southwest "slum" off 4th Street, around 1910. Image by Library of Congress licensed under Creative Commons.

While this system was formally established in 1937, the Housing Act of 1949 accelerated these efforts as part of a larger package of programs that set the goal of “a decent home and a suitable living environment for every American family.”

The law consolidated public housing with other slum clearance housing programs, including the precursor to Urban Renewal, and dedicated funds to build up to 810,000 units of public housing nationwide by 1955. However, that goal was undermined in the same law, which also permitted housing segregation, capped federal contributions to public housing, and shrunk federal subsidy periods from 60 to 40 years.

Additionally, both the 1937 and the 1949 laws placed a ceiling on construction costs per room, disincentivizing use of quality materials despite the inclusion of modern appliances, and restricted use of annual federal disbursements to only cover the difference between operations needs and rent revenue.

The dawn of federal disinvestment

The next presidential administration had further reduced federal funds for public housing construction. Meanwhile, although hundreds of thousands of public housing units had been built by this time, the lack of continued investment in maintenance of public housing led to rapid deterioration.

From the outset, the federal government left maintenance funding and procedures up to each of the local housing authorities, presuming that rental revenue at each development would cover maintenance costs.

Housing authorities, which tasked third-party property management companies with overseeing repairs, were able to blame lack of federal funds or mismanagement for lax or inconsistent upkeep, and management companies could point to low rental revenue to justify deferred maintenance.

The rental revenue gap was widened further as households were forced to move once their incomes exceeded maximum requirements, perpetuating concentration of poor households together. Neglected maintenance and stringent regulations led to public housing replicating the same issues seen in the slums that housing was meant to replace.

In tandem with public housing residents enduring the reality of slumlord behavior from housing authorities, they also had to endure stigmatization and negative public perception. Along with general disdain for low-income people, federal investment in suburban homeownership solidified the white middle class and exacerbated housing segregation, particularly by backing affordable mortgages in areas with restrictive deed covenants.

This process cemented in the public’s imagination an association of Black people with the rundown highrises of the inner-city and white people with the curated sprawl of the suburbs. Housing segregation was similarly pronounced within DC, where land with restrictive covenants occasionally abutted whites-only public housing.

Map of restricted lots and segregated public housing sites, courtesy of Prologue DC.

By the 1960s, the federal government began exploring different means of subsidizing housing rather than investing in new construction, including such approaches as permitting local housing authorities to rent units from private owners to sublet to households that would qualify for public housing, or letting housing authorities purchase newly-completed buildings directly from developers.

In the meantime, however, no innovative approaches to low-income housing could stem the tide of public intellectuals that frowned upon public housing and media coverage that sensationalized crime incidents.

Notably, influential journalist and urban sociologist Jane Jacobs cited several anecdotal examples of crime in public housing in her germinal 1961 textThe Life and Death of Great American Cities, criticizing the slum clearance system and advocating instead for mixed-income, low-density developments.

“Both of these operations, “renewal” projects and public housing projects, with their wholesale destruction, are inherently wasteful ways of rebuilding cities, and in comparison with their full costs make pathetic contributions to city values,” Jacobs wrote. “Project building as a form of city transformation makes no more sense financially than it does socially.”

A few years later, Assistant Secretary of Labor Daniel Patrick Moynihan released “The Negro Family: The Case for National Action” (better known as the Moynihan Report), a text that shaped opinion on the plight of Black America for decades to come. While the report acknowledged the legacy of racism and enslavement, it also added fuel to stereotypes blaming single-parent households for crime and poverty, arguing that if more children were born into wedlock and in houses with employed fathers, there would be less welfare dependence. Moynihan also became known for recommending “benign neglect”of Black households after the 1968 riots leveled city corridors nationwide following the assassination of Martin Luther King, Jr.

“The Biggest Slumlord in History”

But the pendulum swung decidedly in favor of divesting from public housing in January 1973, when the secretary of the Department of Housing and Urban Development (HUD) George Romney, despite his personal opinions and under the direction of then-President Richard Nixon, announced an 18-month moratorium on slum clearance-and-development projects and new production of subsidized housing.

While this rule change was ostensibly to give HUD the opportunity to study and reform the public housing system to shift more responsibility for funding and construction to local authorities, it ended up doing more of the latter than the former.

A report submitted by HUD that year criticized how public housing was financed, noted inconsistencies among the standards within and enforcement of building codes nationwide, and highlighting the inefficiencies of federal housing policy toward low-income households.

By that fall, Nixon was declaring federal housing programs a failure, parroting mainstream characterizations by arguing that it was “wasteful” to build new housing for low-income households. In an address to Congress in September of 1973, Nixon further derided the existing public housing system, citing it as a failed experiment.

“I have seen a number of our public housing projects. Some of them are impressive, but too many are monstrous, depressing places—run down, overcrowded, crime-ridden, falling apart. The residents of these projects are often strangers to one another—with little sense of belonging. And because so many poor people are so heavily concentrated in these projects, they often feel cut off from the mainstream of American life….All across America, the Federal Government has become the biggest slumlord in history.”

A pivot from public housing to housing subsidies

Nixon insisted on a pivot toward giving low-income households voucher subsidies so they could find their own housing. Although this concept wasn’t broadly accepted at the time, it was enough to swing momentum to diversion of funds from construction and maintenance of public housing.

Public disdain toward government “giveaways” was further inflamed by images of the “welfare queen” in the late 1970s, which made the idea of simply subsidizing existing rental units more politically palatable over the two decades that followed. Mismanagement of federal funds by local housing authorities also cast doubt on the efficiency of spending more on public housing.

The District’s then-Department of Public and Assisted Housing (DPAH; now DC Housing Authority) was no exception: in 1977, DPAH requested and received funds from HUD to renovate 28 units deemed uninhabitable at the (one-time whites-only) Fort Dupont public housing community. Four years later, the funds remained unspent and rising costs led DPAH to request demolition of those units instead. After another two years, the demolition request increased to 112 units, and residents had already begun moving out or were threatened with eviction.

The debacle led residents to file a lawsuit (Edwards v. District of Columbia) which shone a light on the practice of demolition becoming a necessity due to willful neglect of housing maintenance.

Fort Dupont Houses by Library of Congress, Prints & Photographs Division, Gottscho-Schleisner Collection licensed under Creative Commons.

HUD’s complicity in delaying consideration of DPAH’s initial demolition requests indicates the federal government’s shift in priorities, as HUD began testing out new means to relieve local public housing authorities from the financial pressures associated with housing low-income families. One of those means was the creation of Low Income Housing Tax Credits (LIHTC) in 1986, which use taxes to incentivize the construction and renovation of affordable housing. These were first used in DC to build Atlantic Terrace in Washington Highlands and to update the historic Mayfair Mansions workforce housing development in Northeast. LIHTC has since grown to become the most prevalent source of affordable housing units nationwide.

The 1990s was primarily marked by establishing a series of programs meant to reform the housing system, including HOPE VI, which awarded federal grants to replace public housing with mixed-income units, and Moving to Work (MTW), which gives some housing authorities more flexibility to experiment with federal funds. In DC, HOPE VI kicked off with the construction of the Townhomes at Capitol Hill on the former site of the Ellen Wilson Dwellings, and MTW has primarily been used to cover operating expenses and subsidize vouchers in more submarkets citywide.

By then, the DC Housing Authority could not begin implementing subsidies and renovations fast enough — after all, HUD had graded the city’s public housing portfolio a 22.38 on a 100-point scale, identifying 2,000 out of roughly 11,000 units as inhabitable in a 1992 audit.

As a result of the pivot to redevelopments and the increased reliance on vouchers, over 250,000 public housing units nationwide (and over 4,000 in DC in the past three decades) have been demolished or converted via subsidies, federal funds for public housing have steadily decreased, and negative public perception of subsidized housing has become further entrenched. Between 2002 and 2017, federal dollars for both maintenance (via the Public Housing Operating Fund) and renovations (via the Public Housing Capital Fund) decreased in all but two fiscal years.

A 2010 HUD study noted a nationwide backlog of $26 billion in capital funds; the DC Housing Authority more recently cited the need for $1.3 billion to bring its portfolio up to standard. That public housing was allowed to fail is the cumulative effect of decades of public disdain toward, federal disinvestment from, and poor mismanagement of public housing.